In the early 2000s, everything was changing: We had the dot-com bust, the advent of the smartphone, and the rise of ecommerce. People were using the Euro, PayPal, and – for the first time – more laptops than PCs.

In this world, in the Netherlands, to be precise, a consortium of major banks – ABN AMRO, ING, Rabobank, and others – came together to create a system that would define the Dutch payments landscape for years to come: iDEAL payments.

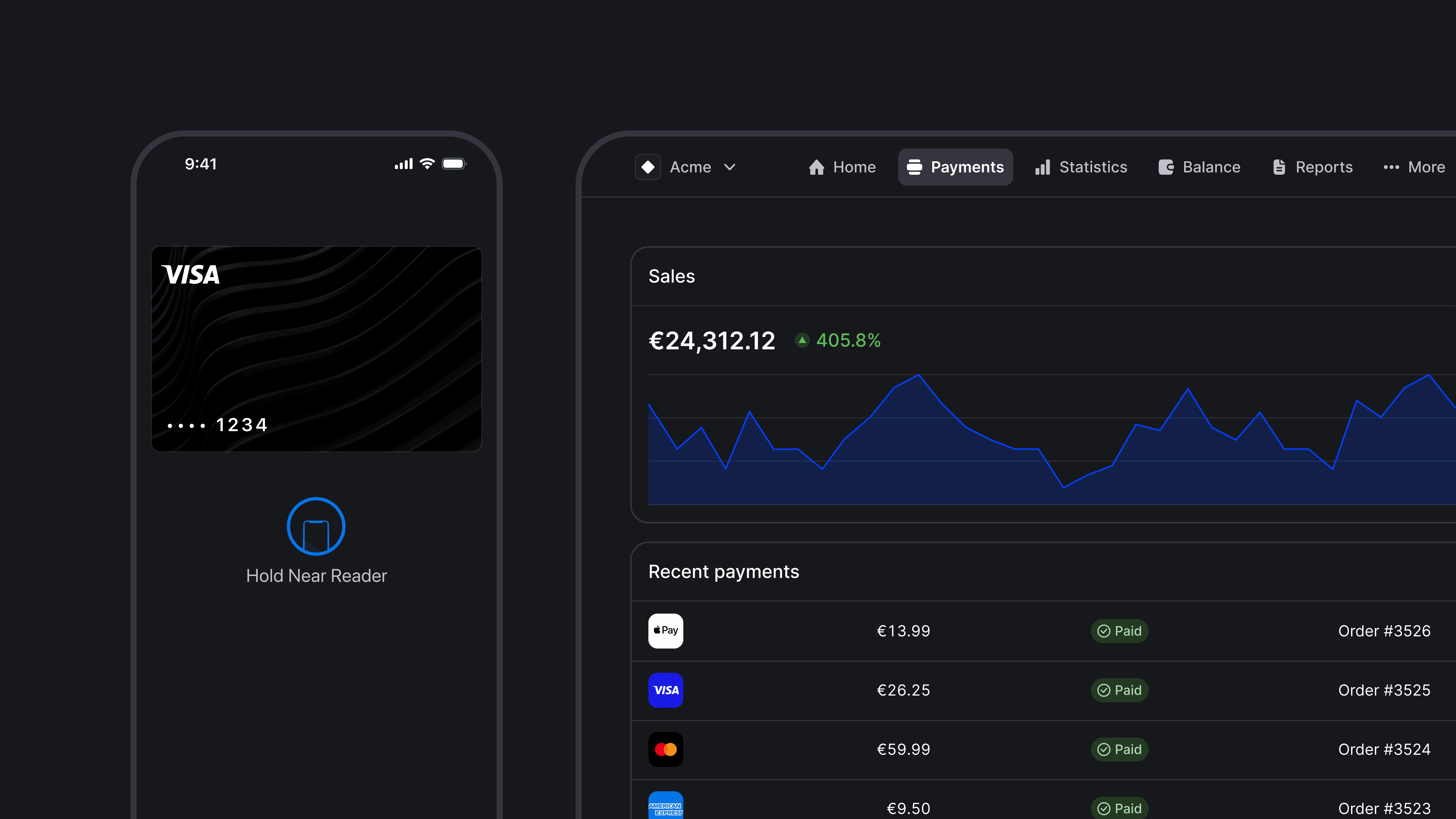

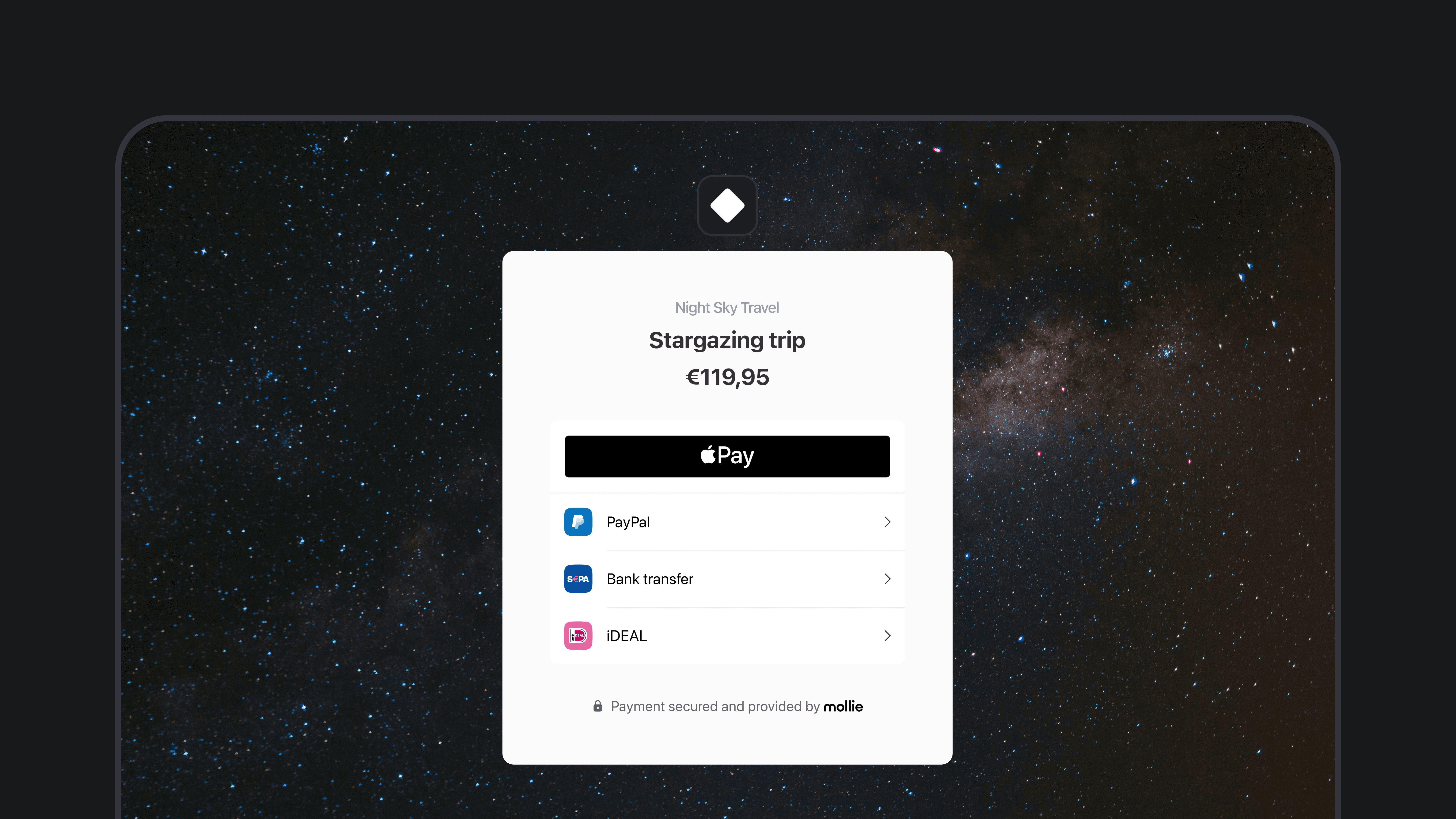

Launched in 2004, iDEAL provides a secure, convenient, and accessible way to pay online. Just a year after launch, it hit the one million transaction milestone. Now, two decades later, it dominates the online payments space, powering more than 70% of the country’s online purchases.

But things are changing. Or, more specifically, the Dutch payments landscape is fragmenting: new players are emerging and gaining market share, technology is disrupting how we shop and buy, and more consumers are using cards and wallets to pay.

It’s almost impossible to predict the future. But it is possible to point out the signs that show where we might end up. Here, our Head of Payments, Iryna Agieieva, does just that, exploring some of the key initiatives and evolutions shaping the future of payments in the Netherlands.

In the early 2000s, everything was changing: We had the dot-com bust, the advent of the smartphone, and the rise of ecommerce. People were using the Euro, PayPal, and – for the first time – more laptops than PCs.

In this world, in the Netherlands, to be precise, a consortium of major banks – ABN AMRO, ING, Rabobank, and others – came together to create a system that would define the Dutch payments landscape for years to come: iDEAL payments.

Launched in 2004, iDEAL provides a secure, convenient, and accessible way to pay online. Just a year after launch, it hit the one million transaction milestone. Now, two decades later, it dominates the online payments space, powering more than 70% of the country’s online purchases.

But things are changing. Or, more specifically, the Dutch payments landscape is fragmenting: new players are emerging and gaining market share, technology is disrupting how we shop and buy, and more consumers are using cards and wallets to pay.

It’s almost impossible to predict the future. But it is possible to point out the signs that show where we might end up. Here, our Head of Payments, Iryna Agieieva, does just that, exploring some of the key initiatives and evolutions shaping the future of payments in the Netherlands.

In the early 2000s, everything was changing: We had the dot-com bust, the advent of the smartphone, and the rise of ecommerce. People were using the Euro, PayPal, and – for the first time – more laptops than PCs.

In this world, in the Netherlands, to be precise, a consortium of major banks – ABN AMRO, ING, Rabobank, and others – came together to create a system that would define the Dutch payments landscape for years to come: iDEAL payments.

Launched in 2004, iDEAL provides a secure, convenient, and accessible way to pay online. Just a year after launch, it hit the one million transaction milestone. Now, two decades later, it dominates the online payments space, powering more than 70% of the country’s online purchases.

But things are changing. Or, more specifically, the Dutch payments landscape is fragmenting: new players are emerging and gaining market share, technology is disrupting how we shop and buy, and more consumers are using cards and wallets to pay.

It’s almost impossible to predict the future. But it is possible to point out the signs that show where we might end up. Here, our Head of Payments, Iryna Agieieva, does just that, exploring some of the key initiatives and evolutions shaping the future of payments in the Netherlands.

In the early 2000s, everything was changing: We had the dot-com bust, the advent of the smartphone, and the rise of ecommerce. People were using the Euro, PayPal, and – for the first time – more laptops than PCs.

In this world, in the Netherlands, to be precise, a consortium of major banks – ABN AMRO, ING, Rabobank, and others – came together to create a system that would define the Dutch payments landscape for years to come: iDEAL payments.

Launched in 2004, iDEAL provides a secure, convenient, and accessible way to pay online. Just a year after launch, it hit the one million transaction milestone. Now, two decades later, it dominates the online payments space, powering more than 70% of the country’s online purchases.

But things are changing. Or, more specifically, the Dutch payments landscape is fragmenting: new players are emerging and gaining market share, technology is disrupting how we shop and buy, and more consumers are using cards and wallets to pay.

It’s almost impossible to predict the future. But it is possible to point out the signs that show where we might end up. Here, our Head of Payments, Iryna Agieieva, does just that, exploring some of the key initiatives and evolutions shaping the future of payments in the Netherlands.