You’re scaling across Europe, but your finance team is still manually chasing invoices. If your business relies on recurring revenue, waiting for customers to manually authorise payments costs you time, money and predictability.

Relying on manual bank transfers and credit cards creates compounding risks for your business:

Bloated days sales outstanding (DSO): Waiting on manual bank transfers ties up your working capital and fractures your cash flow forecasting.

Involuntary churn: When corporate credit cards expire or fail, you risk losing perfectly loyal subscribers to administrative friction.

Reconciliation nightmares: Your finance team is wasting valuable hours matching disparate batch files to invoices – instead of driving strategic financial planning.

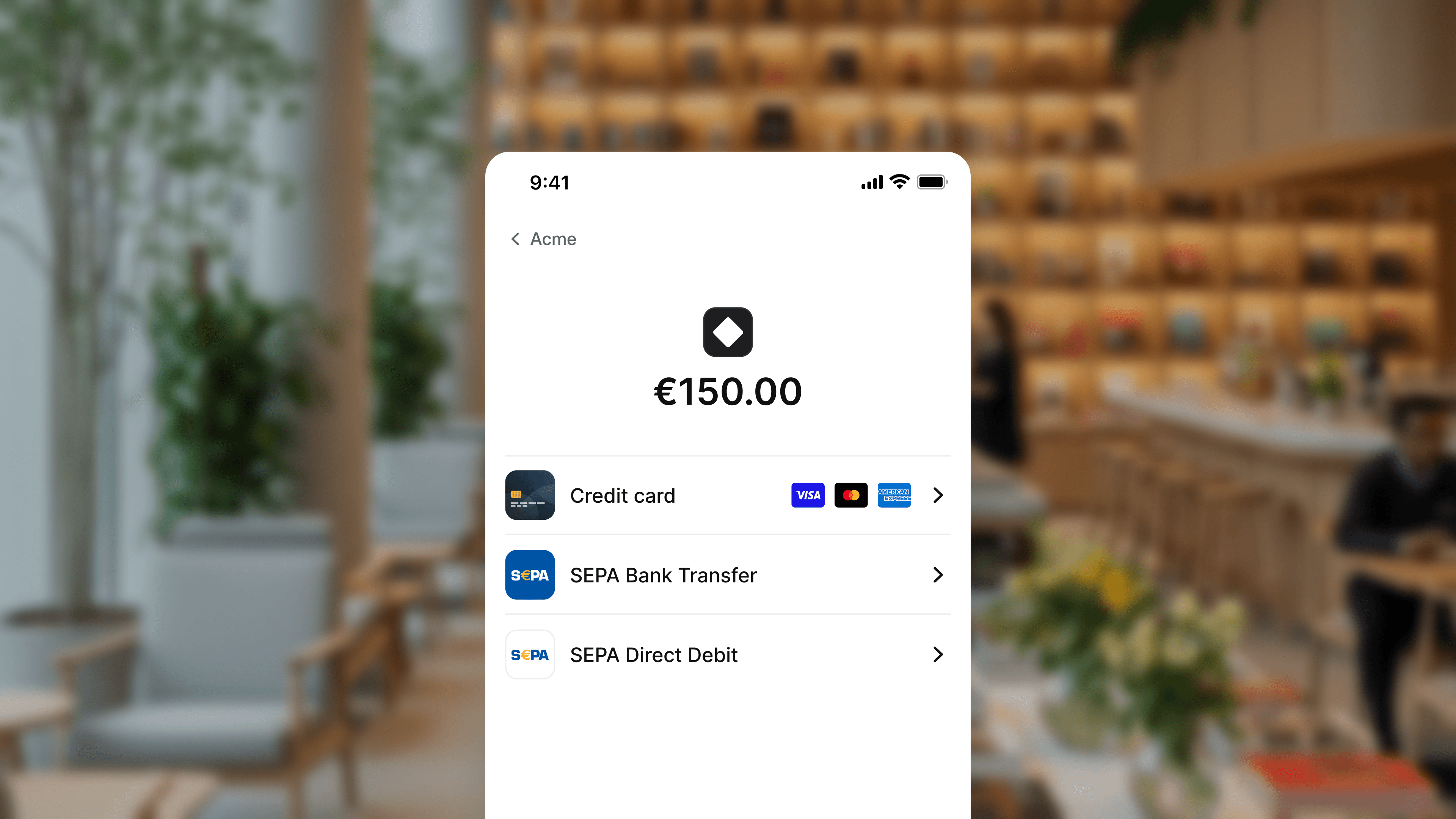

SEPA Direct Debit solves all of this by putting your business in charge of the transaction. Instead of waiting for customers to act, you initiate the collection directly – automating your billing cycle and eliminating the manual overhead that comes with it.

This guide breaks down everything you need to know about SEPA Direct Debit, from how it works and the types of mandates available to the rules governing collections, and the exact steps required to integrate it into your payment stack.

You’re scaling across Europe, but your finance team is still manually chasing invoices. If your business relies on recurring revenue, waiting for customers to manually authorise payments costs you time, money and predictability.

Relying on manual bank transfers and credit cards creates compounding risks for your business:

Bloated days sales outstanding (DSO): Waiting on manual bank transfers ties up your working capital and fractures your cash flow forecasting.

Involuntary churn: When corporate credit cards expire or fail, you risk losing perfectly loyal subscribers to administrative friction.

Reconciliation nightmares: Your finance team is wasting valuable hours matching disparate batch files to invoices – instead of driving strategic financial planning.

SEPA Direct Debit solves all of this by putting your business in charge of the transaction. Instead of waiting for customers to act, you initiate the collection directly – automating your billing cycle and eliminating the manual overhead that comes with it.

This guide breaks down everything you need to know about SEPA Direct Debit, from how it works and the types of mandates available to the rules governing collections, and the exact steps required to integrate it into your payment stack.

You’re scaling across Europe, but your finance team is still manually chasing invoices. If your business relies on recurring revenue, waiting for customers to manually authorise payments costs you time, money and predictability.

Relying on manual bank transfers and credit cards creates compounding risks for your business:

Bloated days sales outstanding (DSO): Waiting on manual bank transfers ties up your working capital and fractures your cash flow forecasting.

Involuntary churn: When corporate credit cards expire or fail, you risk losing perfectly loyal subscribers to administrative friction.

Reconciliation nightmares: Your finance team is wasting valuable hours matching disparate batch files to invoices – instead of driving strategic financial planning.

SEPA Direct Debit solves all of this by putting your business in charge of the transaction. Instead of waiting for customers to act, you initiate the collection directly – automating your billing cycle and eliminating the manual overhead that comes with it.

This guide breaks down everything you need to know about SEPA Direct Debit, from how it works and the types of mandates available to the rules governing collections, and the exact steps required to integrate it into your payment stack.

You’re scaling across Europe, but your finance team is still manually chasing invoices. If your business relies on recurring revenue, waiting for customers to manually authorise payments costs you time, money and predictability.

Relying on manual bank transfers and credit cards creates compounding risks for your business:

Bloated days sales outstanding (DSO): Waiting on manual bank transfers ties up your working capital and fractures your cash flow forecasting.

Involuntary churn: When corporate credit cards expire or fail, you risk losing perfectly loyal subscribers to administrative friction.

Reconciliation nightmares: Your finance team is wasting valuable hours matching disparate batch files to invoices – instead of driving strategic financial planning.

SEPA Direct Debit solves all of this by putting your business in charge of the transaction. Instead of waiting for customers to act, you initiate the collection directly – automating your billing cycle and eliminating the manual overhead that comes with it.

This guide breaks down everything you need to know about SEPA Direct Debit, from how it works and the types of mandates available to the rules governing collections, and the exact steps required to integrate it into your payment stack.